Access full report

Oops! Something went wrong while submitting the form.

🤍

Facilitated by The Modern Data Company in collaboration with the Modern Data 101 Community

Latest reads...

TABLE OF CONTENT

.png)

A bank today is a data business. The problem is that most of its data is trapped.

Every transaction, loan application, fraud alert, and compliance filing generates information that risk and operations teams depend on, but digital expansion has outpaced the architecture meant to carry it. Banks now run across mobile apps, internet banking portals, risk engines, and back-office tools, each generating continuous streams of data, each sitting in its own silo.

The result is a fragmented infrastructure that quietly undermines everything built on top of it: AI programs that can’t scale, risk models working off incomplete pictures, compliance teams stitching together audit trails from four different systems, and IT budgets consumed by maintenance rather than momentum.

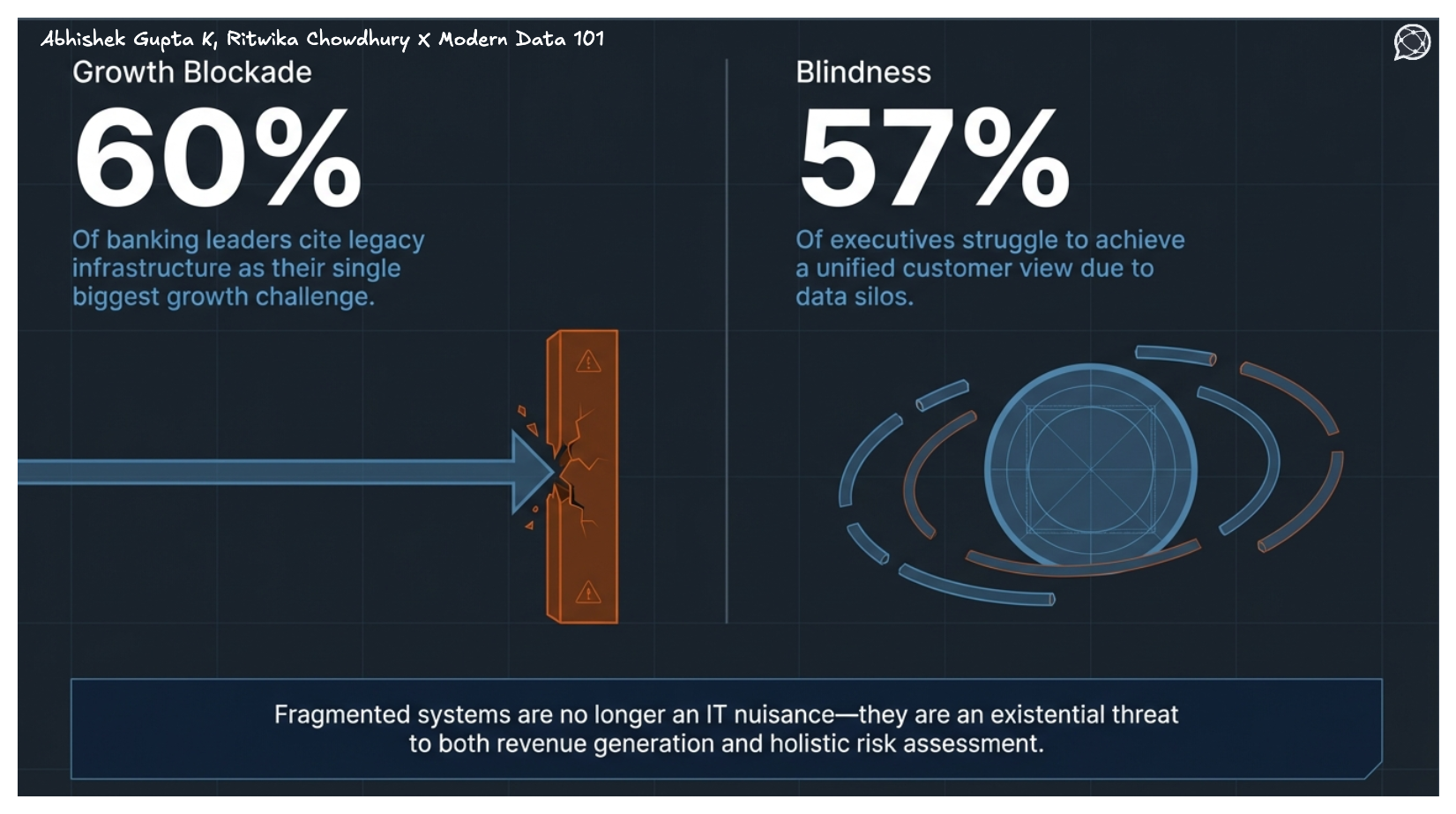

The consequences of fragmentation are wide-ranging. Legacy infrastructure is increasingly cited as a core growth constraint, with nearly 68% of banking leaders saying their current technology architecture is a hindrance to meeting customer needs. At the same time, 57% of banking executives still struggle to achieve a unified customer view due to data silos, making it difficult to assess risk or relationship value holistically.

Banks are now responding with a deliberate move toward unified and converged data platforms: not as an IT upgrade, but as a strategic foundation for risk intelligence, regulatory compliance, and AI-powered decision-making. This article examines what that shift looks like and why it can no longer wait.

Fragmented data systems occur when critical banking information is scattered across disconnected, siloed platforms, often a legacy of mergers, legacy infrastructure, and decentralised decisions.

Most banks operate across multiple disconnected layers: fraud, compliance, customer data, and core operations, each optimised for its own purpose but not designed to work together.

As a result, the same customer is evaluated differently across systems, risk logic is duplicated, and critical signals fail to move across domains in time, reinforcing the blind spots created by organisational silos. A transaction flagged in one system may pass in another without context, or a high-risk customer may still be targeted for growth. This creates a core disconnect: growth systems optimise for speed, while risk systems optimise for control. Fragmentation forces banks to choose, often compromising both.

[related-1]

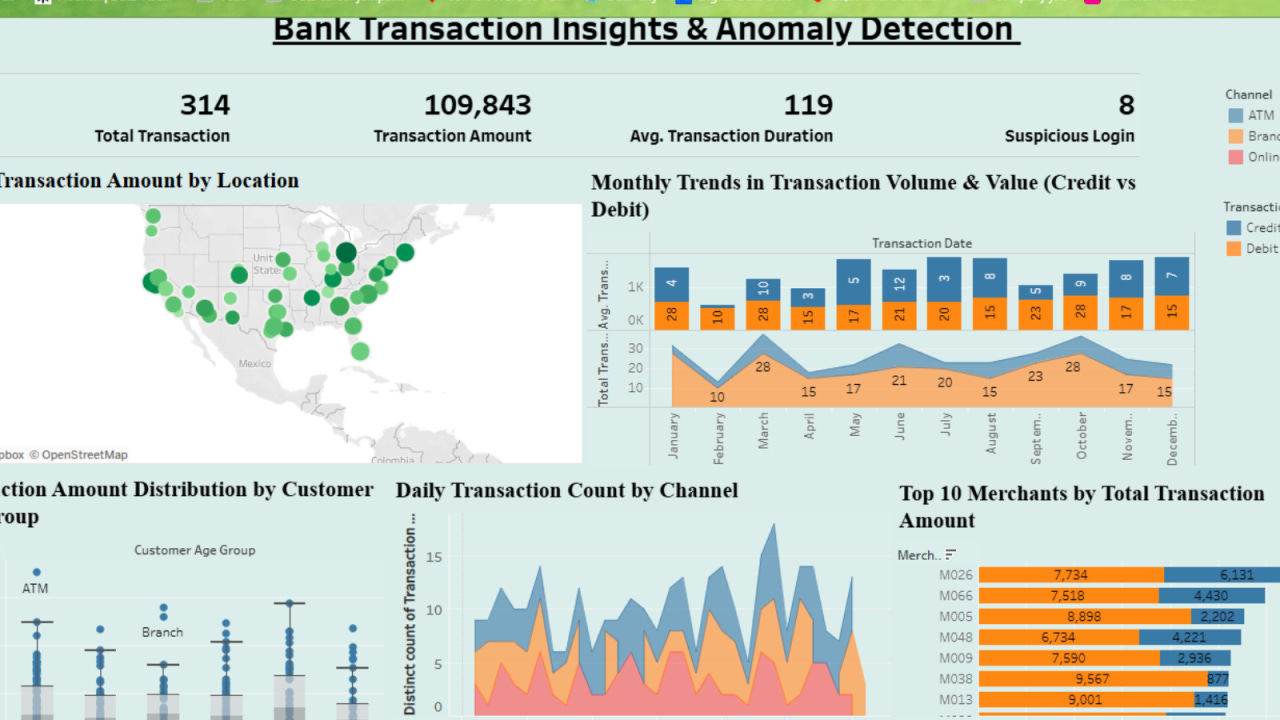

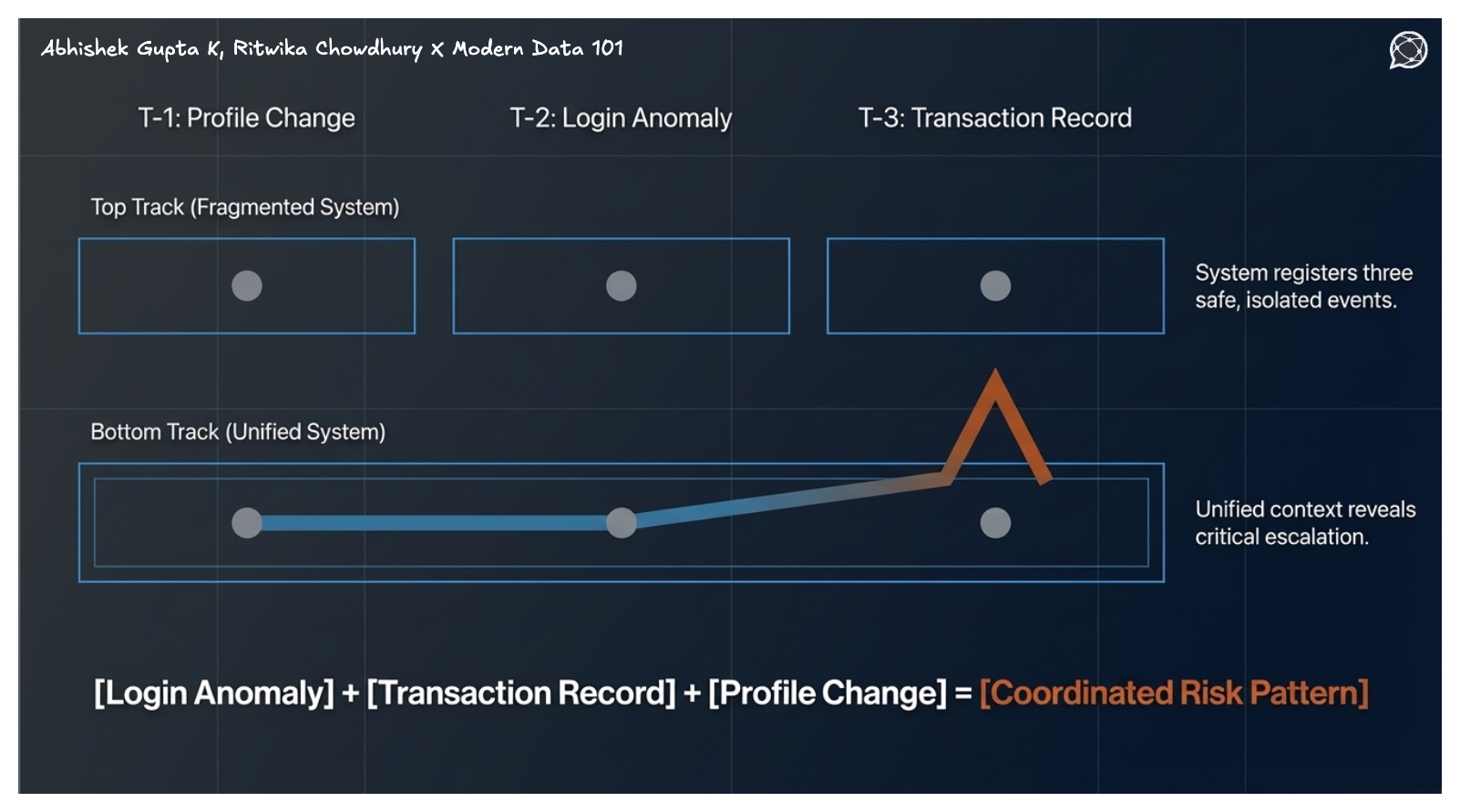

Customer interactions, transaction records, behavioural signals, and third-party risk indicators exist in separate systems. Each dataset holds value independently, but risk emerges from patterns across them. Without unification, a login anomaly goes unlinked to transaction behaviour, a profile change remains disconnected from credit exposure, and fraud signals lack the historical context needed for enrichment.

The result is partial visibility masquerading as genuine insight, banks missing risk signals not because the data doesn't exist, but because it was never connected.

Banking architectures span hybrid cloud environments, API-driven integrations, fintech ecosystems, and event-driven microservices. Every integration is a potential failure point, every API a vulnerability, every data movement a source of latency and inconsistency.

What was built for agility increasingly produces entropy. Teams spend more time reconciling data and debugging inconsistencies than anticipating threats or modelling risk. The architecture, meant to enable intelligence, becomes a source of risk itself.

[related-2]

A unified data platform is a single operating layer that connects fragmented systems, channels, and data into one place, giving every team and every AI agent one consistent source of truth.

As most banks run on several disconnected applications: separate tools for mobile banking, loan origination, call centre operations, fraud detection, and compliance reporting, none of which were built to share data with each other.

Unified or converged data platforms sit above legacy core infrastructure, using API orchestration to connect everything underneath. Banks retain their existing investments while gaining a unifying layer that makes disparate systems behave as one. These platforms merge transactional processing, analytical queries, and real-time data processing and streaming into a single architecture that handles all three simultaneously, eliminating the latency that typically exists between data generation and decision-making.

[related-3]

Starting with just a small example.

Think of these unified and converged data platforms in a security context. Rather than routing fraud signals through one system and compliance telemetry through another, a converged architecture ingests, correlates, and acts on all of it in real time from one place.

Several banks have already started leveraging unified systems and their capabilities to address the root cause of broken risk visibility. Most of these problems occur due to architectural loopholes and disconnected systems with no shared context.

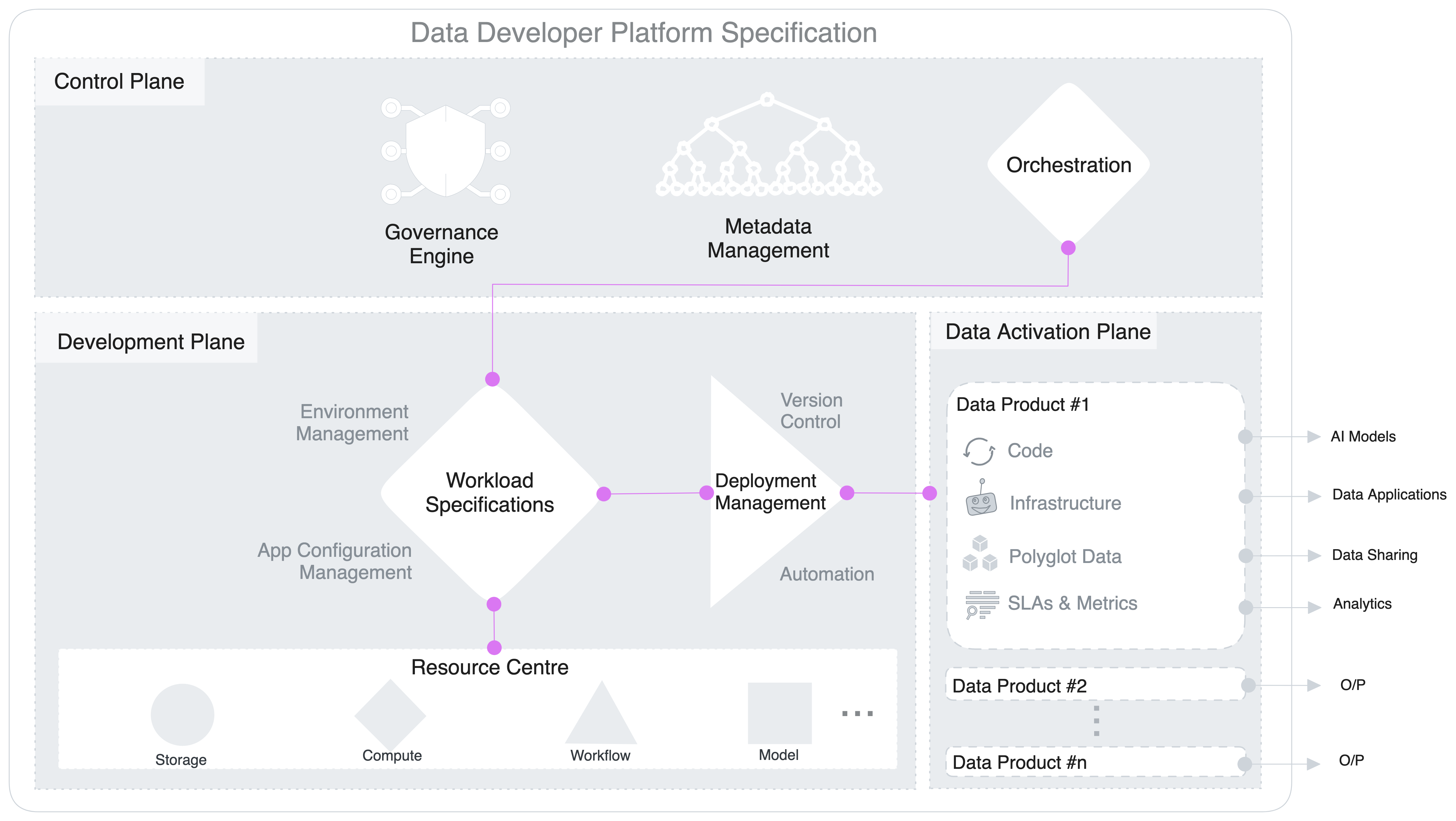

The concept of unified platforms is used in the design of different kinds of data platforms to deliver the business outcome. A data developer platform is built on principles of software engineering, remodelled for the data space. The data developer platform spec is an open, community-driven standard that evolves with the needs of data engineering teams, and is not tied to a single vendor's roadmap. It is purpose-built for data engineering teams, the way an Internal Developer Platform (IDP) is built for software engineers.

1. Unified Governance Across Risk Silos

The Control Plane governs the entire data ecosystem through centralised metadata management, policy-based access control, and orchestration of data workloads, meaning risk-relevant data from core banking, CRM, fraud systems, and behavioural analytics can all be governed under a single, consistent policy framework. No more isolated ownership, no more governance gaps between silos.

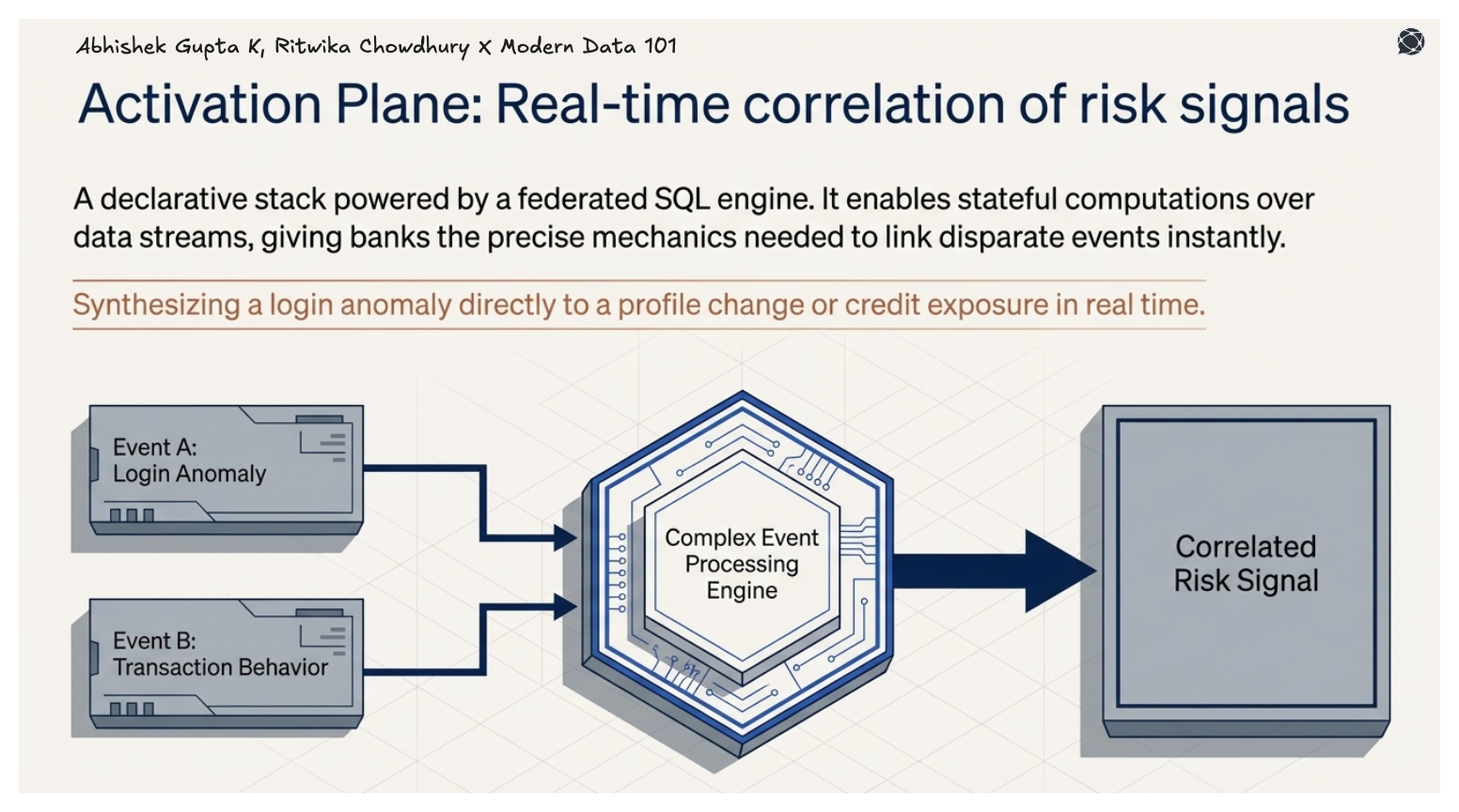

2. Real-Time Correlation of Risk Signals

The Data Activation Plane provides a federated SQL query engine, a complex event processing engine for stateful computations over data streams, and a declarative stack to ingest, process, and syndicate data, precisely what banks need to correlate a login anomaly with transaction behaviour, or link a profile change to credit exposure, in real time.

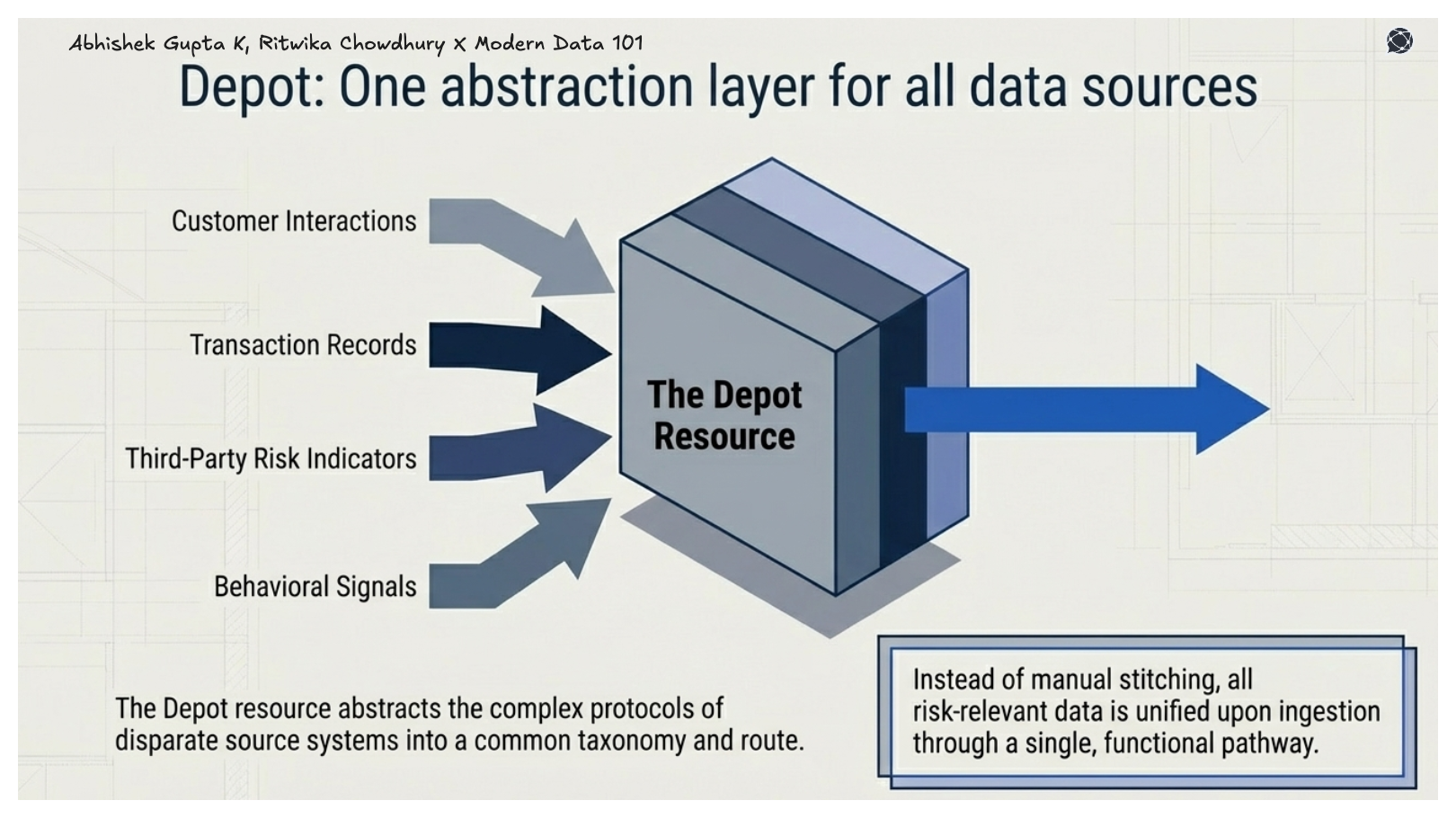

3. One Abstraction Layer for All Data Sources

Critically, DDP uses a Depot resource, which is a uniform way to connect to various data sources, simplifying the process by abstracting the various protocols and complexities of source systems into a common taxonomy and route.

For banks, this means customer interaction data, transaction records, third-party risk indicators, and behavioural signals can all be ingested through a single abstraction layer, unified, not stitched together manually.

4. Unified Architecture Without Fragmentation Overhead

The layered kernel architecture promotes a unified experience as opposed to the complexity overheads of a microservices architecture, a loosely coupled yet tightly integrated set of components that eliminates the performance and maintenance drag that fragmented banking stacks typically carry.

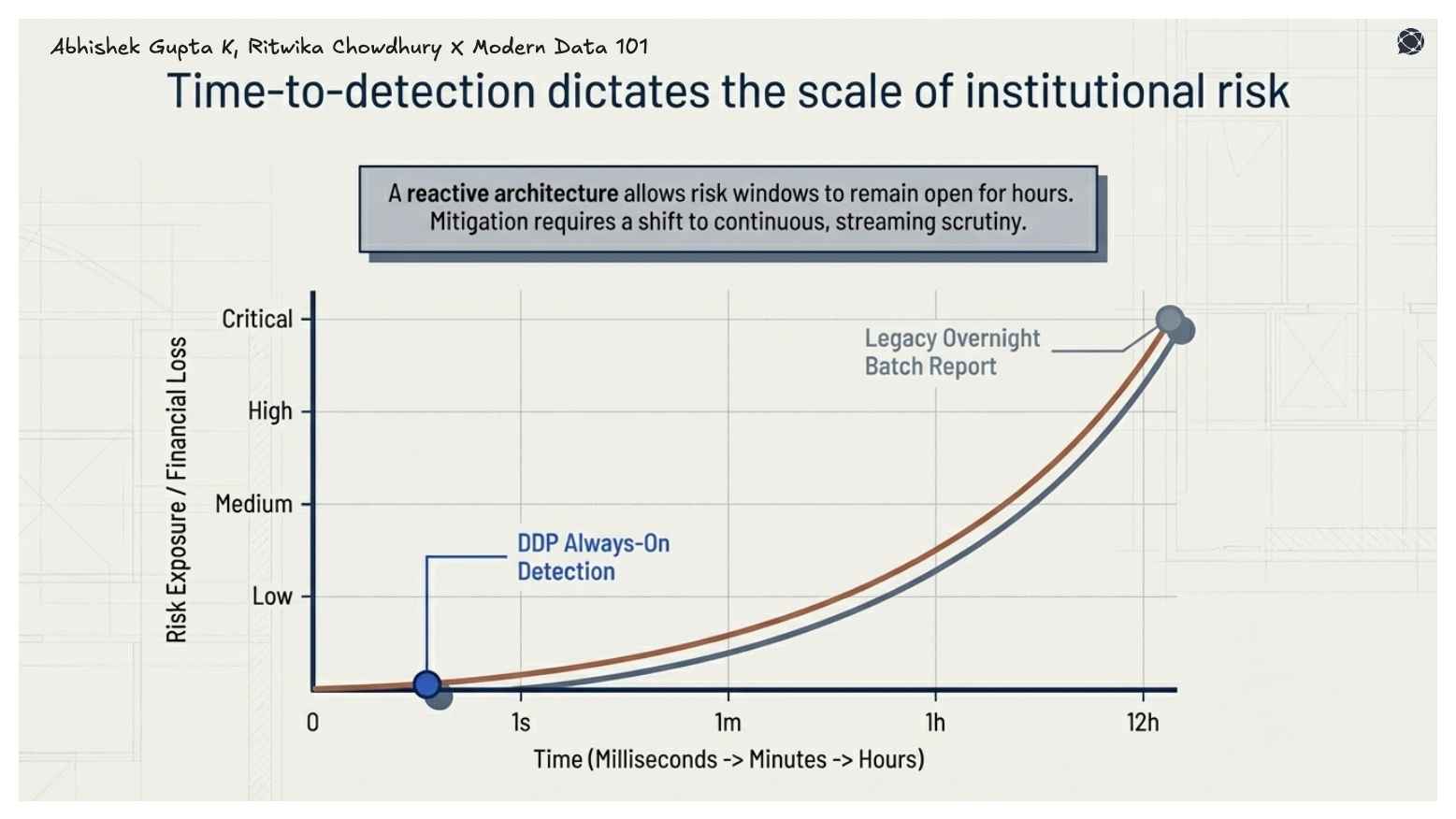

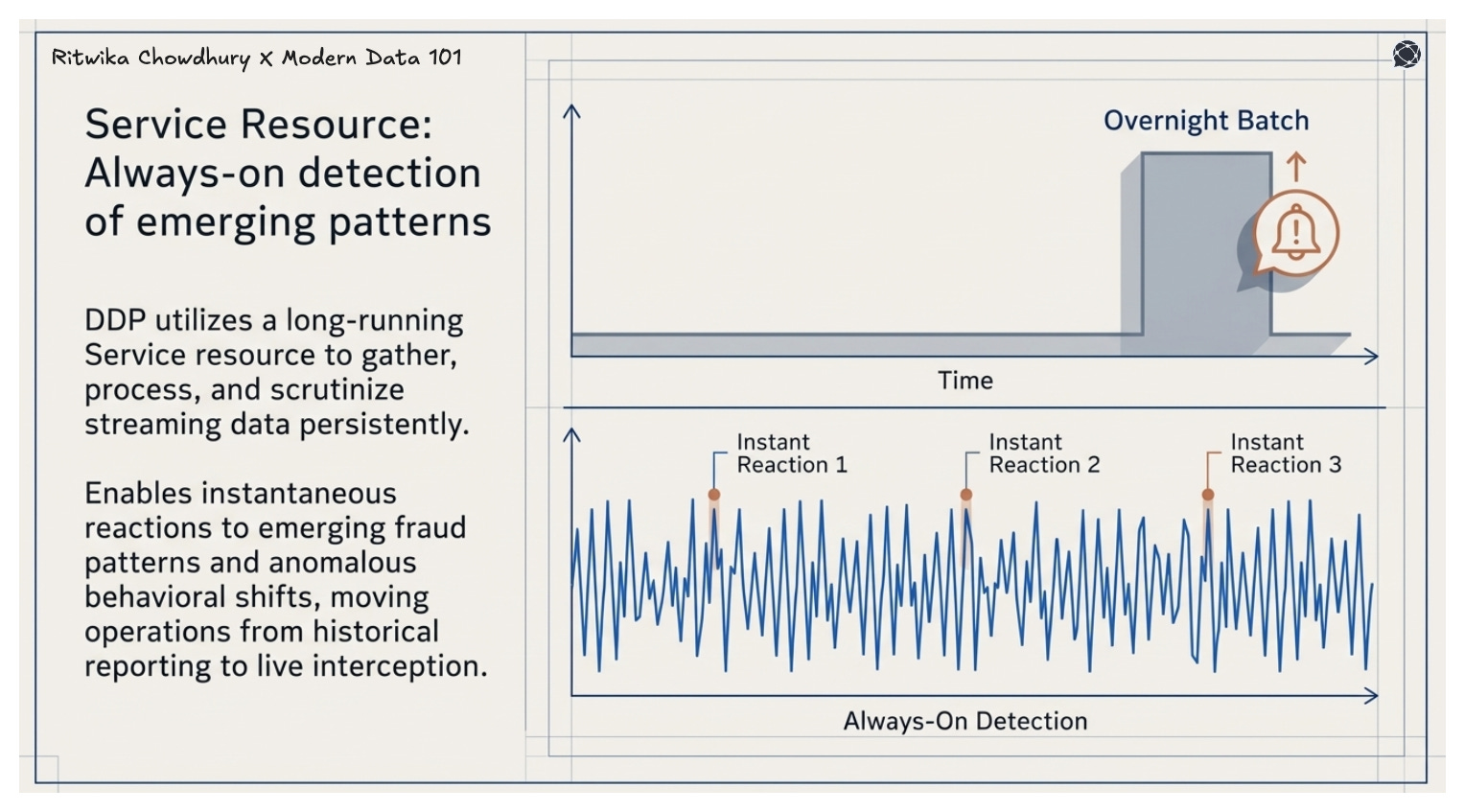

5. Always-On Detection of Emerging Risk Patterns

On risk patterns specifically, DDP’s Service resource, a long-running process that gathers, processes, and scrutinises streaming data for quick reactions, which enables banks to detect emerging fraud patterns or anomalous behavioural shifts in real time, rather than discovering them in outputs from batch processing systems when it’s already too late.

Customer data travels with the customer across mobile, web, branch, and call centre. Context-aware interactions reduce drop-off and drive loyalty.

Configuration over custom builds enables new products that can be launched in weeks rather than nine to twelve months, along with pre-built journeys for account opening, loan origination, and onboarding

Unified platforms offer an end-to-end and unified view of all customer data, enabling next-best-action recommendations in real time. Banks report 25–50% cross-sell gains with unified platforms

Customer insights are incredibly important for financial institutions, and unified platforms help here by eliminating toggling between five or six systems to answer a simple customer question. They also help transform frontline staff from data entry clerks into advisors.

Clean, connected data is a prerequisite for AI agents to operate safely and reliably. Banks with unified platforms can move AI from experimental pilots to full production.

However, most banks are still far from being future-ready, with the gap largely rooted in fragmented data infrastructure.

A key shift enabled by a Data Developer Platform is the move from pipelines to data products.

Instead of building one-off pipelines for fraud, compliance, or credit risk, banks define reusable, governed data products such as customer risk profiles, transaction intelligence streams, or behavioural risk signals. Data products are packaged with logic, quality, access policies, and lineage, making them directly usable across teams.

In a fragmented setup, the same risk logic is rebuilt across systems. With data products, it is defined once and reused everywhere, whether for fraud detection, AML monitoring, or credit decisioning.

This changes how risk intelligence operates. Risk signals become composable building blocks, not isolated outputs. Teams consume trusted, ready-to-use data, not raw pipelines, and AI models and decision systems operate on consistent, shared context.

A unified banking platform connects core banking, customer data, fraud, compliance, and analytics into a single shared data and decision layer.

It replaces silos with real-time data sharing, consistent decisions, and federated governance, turning fragmented systems into a coordinated platform for decisions.

The 7 Ps of banking refer to the extended marketing mix used in financial services:

These define how banks design, deliver, and differentiate their services.

The 4 pillars of a risk-based approach (commonly in banking/AML) are:

These pillars ensure risk is prioritised, controlled, and continuously managed.

Your Copy of the Modern Data Survey Report

Better decisions start with shared insight.

Pass it along to your team →

Your Copy of the Modern Data Survey Report

Better decisions start with shared insight.

Pass it along to your team →

Find more community resources

Modern Data 101 is a movement redefining how the world thinks about data. A community built by the same team behind the world’s first data operating system, Modern Data 101 sits at the intersection of data, product thinking, and AI. Spread across 150+ countries, the community brings together a global network of practitioners, architects, and leaders who are actively building the next generation of data systems.

At its core, Modern Data 101 exists to simplify the journey from raw data to tangible and observable impact. It advocates high-potential data systems and next-gen architectures to unify and activate insights and automation across analytics, applications, and operational workflows at the edge.

In a world shifting from data stacks to AI ecosystems, Modern Data 101 helps teams not just navigate the change but lead it.

Find all things data products, be it strategy, implementation, or a directory of top data product experts & their insights to learn from.

Connect with the minds shaping the future of data. Modern Data 101 is your gateway to share ideas and build relationships that drive innovation.

Showcase your expertise and stand out in a community of like-minded professionals. Share your journey, insights, and solutions with peers and industry leaders.